Matt's Minutes (Vol. 2): Is SaaS Dead ☠️😵🪦?

and do we need to get back to building real things?

Happy Friday everyone - As the global fascination with LK-99 continues to surge - a topic I delved into in my previous article - we find ourselves living in an exciting time marked by a "New Era Revolution" that is taking place with massive improvements in technologies like Artificial Intelligence and material science.

In light of these developments, an important question arises 🧐:

Are we witnessing the beginning of a transformative shift from funding software startups to something else? (and no not AI either)

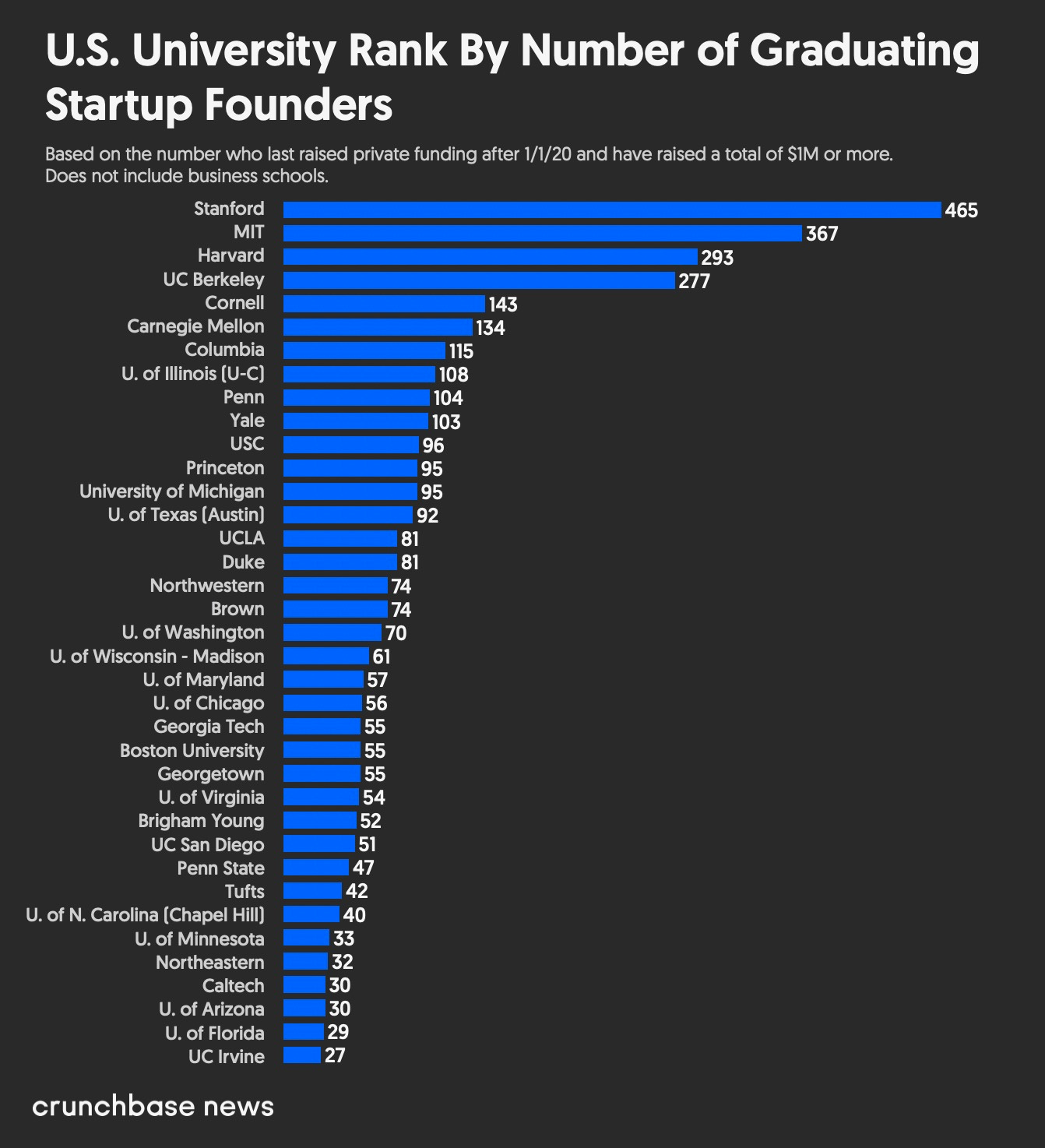

In recent years, venture capitalists have predominantly directed their investments toward software startups initiated by graduates of Stanford and MIT.

However, with the rise in interest in LK-99 and GPU computing to scale AI, it looks like hardware startups may provide the most value in the coming future. Moreover, I was curious in assessing the value software companies have had over the past decade compared to hardware companies.

Is there something wrong with software startups?

Most of the ventures over the past decade have primarily focused on startups that make incremental changes to already existing platforms. Some examples of these startups include Slack, Patreon, Grammarly, and DocuSign which have only made small improvements when compared to the technological breakthroughs SpaceX and Tesla have made. For example, SpaceX developed the first reusable rocket and Tesla innovated the first commercially-successful electric car.

So what? There are still software companies like Google and Meta that are very successful.

Fair, let's talk about the big dogs then. There have been numerous software companies that have revolutionized and made drastic improvements to humanity such as the success of Google, Microsoft, and Meta. However, mimetic theory in combination with the stagnation effect suggests that software companies have become increasingly exhaustive. Essentially, nobody can recreate Google again since it has already been created.

Stagnation Effect: Essentially, a critique of humanity’s immense strides in insignificant software innovation, while other sectors of the economy have experienced limited progress.

Over the past decade, we really only witnessed digital advancements that led to increased smartphone addiction without major enhancements to our daily lives. Think of the different social media platforms we use today and if they truly enhanced humanity versus advancements in space exploration and cleaner energy.

Mimetic Theory: Best explained as a psychological theory that suggests people do things based on other people’s success. Think “sheep following the herd.” In Silicon Valley, this effect takes place as we see everyone wanting to go into software because of the recent success of software companies (like Google and Amazon) post the dot-com crash.

So what? Slack, Patreon, and Grammarly make money and that’s all that matters right?

Actually, the startups listed above have yet to achieve profitability. While these companies have reached massive growth, there are a number of reasons why most software startups struggle to become profitable - which I get into below ⬇️

So you’re saying software companies aren’t good investments?

Kinda, but not exactly – We already know the importance that hardware has on software. For example, AI has only reached the advancement it has due to breakthroughs in hardware, such as GPU technology with Nvidea’s A100s to train these complex AI models.

While most software companies have been great plays (Copy.AI, TikTok, Salesforce, etc…), I don’t think that software is more profitable than hardware in all cases. In fact, I believe that true Internal Rate of Return (IRR) is found in hardware.

IRR: Essentially, a financial metric used to measure the performance of an investment over a specific period of time.

As The Dictator himself, Chamath Palihapitiya said recently in the All In Podcast,

“The problem is that most software companies have still not achieved profitability. So, the idea that software businesses generate long-term profits has so far been false.”

Here are the reasons:

Customer Acquisition Costs Are Too High

Early on, software customer growth is often prioritized over profits. This leads to massive spending on sales, marketing, and promotions with a median of 41% of revenue spent on only sales & marketing.

41% of revenue is spent on sales & marketing - Source: Meritech Also, payback periods typically end up being much longer than expected, exceeding 2-3 years. Essentially meaning, it takes way longer than what is expected to make money off of users and achieve profitability.

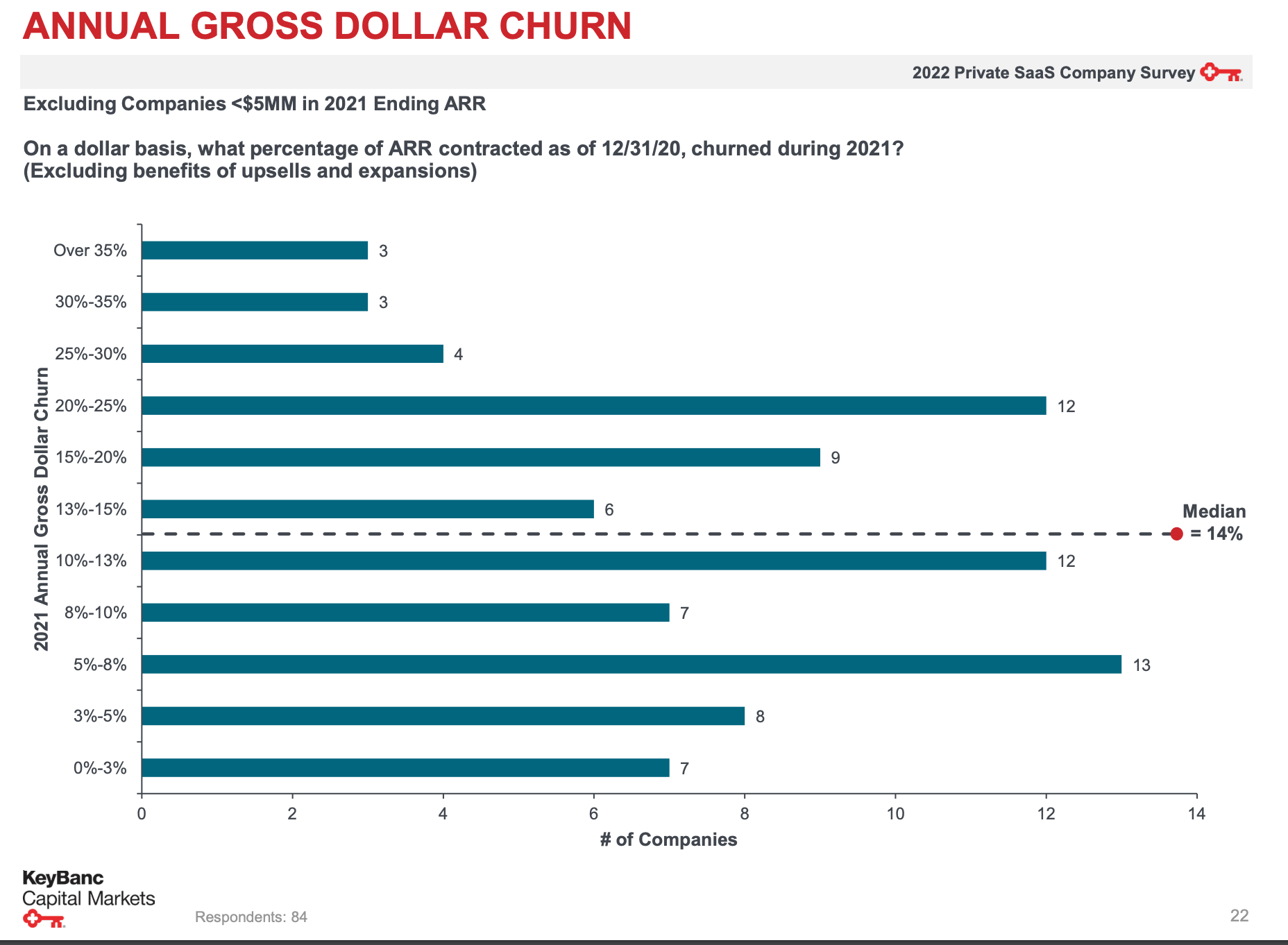

Maintaining Pricing Power is Challenging

Software markets tend to get crowded quickly, leading to intense competition on pricing. Because software companies typically have lower barriers to entry than hardware companies, it makes it hard for software companies to sustain pricing power since users have more options. This limits profit margins and increases churn.

Annual Gross Dollar Churn - Source: KeyBlanc

R&D must remain high to keep products competitive and prevent churn

Software companies require continuous R&D spending to match new features that competitors release. Without constant product innovation and improvements, users will churn to rival platforms. This R&D burden never ends as the pace of software innovation is so fast. It's a constant cash burn.

In conclusion, while software companies have seen tremendous growth over the past decade, I believe there are strong arguments that show very challenging unit economics for long-term profitability when compared to hardware companies.

Between customer acquisition costs, constant pricing pressure, and an endless R&D cycle, software profit margins face constant downward pressure, making hardware possibly more attractive in the coming future.

Startups that caught my eye:

NanoPattern, a Chicago based startup, developing a photo patternable quantum dot formulation to enable the next generation of displays. Raised $1.4M in grants.

Why this is interesting: Nanopattern is developing breakthrough nanoparticle inks that can enable next-generation displays using quantum dots and MicroLEDs. Their key innovation is a patented resin-free nanoparticle lithography technique that allows high-resolution patterning of quantum dot films. This provides a nanoscale precision in depositing red and green quantum dots as color downconverters, unlocking the potential for ultra-high definition displays. By replacing conventional LCD displays with quantum dot and MicroLED technologies, Nanopattern aims to bring vastly improved color gamut, brightness, contrast, and efficiency to consumer devices like TVs, smartphones, AR/VR headsets, and more. With a talented team spun out of UChicago and grant funding from the NSF, Nanopattern is poised to disrupt the display industry with its novel materials science approach. The ability to cost-effectively manufacture quantum dot and MicroLED displays could drive the next revolution in visual technologies.

Quote of the week:

"To be yourself in a world that is constantly trying to make you something else is the greatest accomplishment."

Ralph Waldo Emerson

Stay true to who you are - don’t always follow the herd.

Have a great weekend!

Interesting takes, a bunch of these arguments are new to me! As a software guy myself, I'd love to disagree with you, but I think a lot of these arguments make intuitive sense. There is so much competition that starting a profitable software company is near impossible, and keeping users happy and preventing churn is getting harder. However, I don't think this is a software industry specific phenomenon. You mentioned Tesla as being a great of example of a successful hardware (cars in this case, but really battery and solar tech) company. It's taken Tesla 20 years of continuous innovation to get to where it is now: barely profitable. I totally agree software is more competitive now than it has ever been. I think the common theme among these successful tech companies (hardware and software) is innovation and iteration. Tesla isn't successful because it's a hardware/auto manufacturer, but because it kept iterating until it built a product far better than the rest of the EV market. The same is true for software: Google and Microsoft haven't stopped innovating and as a result are multi-trillion dollar companies. SaaS isn't dead, but for small startups, the best bet to make real money is just to get acquired.